Economics

Economics is the study of how people and societies allocate limited resources to meet unlimited wants.

Economics is divided into two part : -

1. Microeconomics

2. Macroeconomics

What is an Economy?

- An economy is the system that manages how a society produces, distributes, and consumes goods and services.

- It involves money, trade, labor, and resources to keep things running smoothly.

The 4 Key Sectors of an Economy

Sector

- Household

- Firm

- Government

- External

Role

- People who consume goods & provide labor

- Businesses that produce goods/services

- Provides public services & collects taxes

- Trade with other countries

Example

- A worker buying groceries

- A tech company making smartphones

- Building roads , running schools

- Importing oil , exporting software

OUR SYLLUBUS

- Two Economic Sectors

- Household

- Firm

What is Basic Activities in an Economy ?

Basic activities in an economy refer to the core types of work people engage in to earn money and satisfy their needs.

There are 3 main activities:

1. Production – Making goods or giving services.

Example: A farmer grows rice, a doctor treats patients.

2. Consumption – Using goods and services.

Example: Eating food, using a phone.

3. Distribution – Moving goods from makers to users.

Example : Selling products in shops or delivering online orders.

Types of Goods in the Economy

1. Final Consumer Goods

2. Final Producer Goods

- Durable Goods

- Semi-Durable Goods

- Non-Durable Goods

- Services

1. Final Goods

2. Intermediate Goods

3. Consumption/Consumer Goods

4. Capital Goods

1. Final Goods

These goods have crossed the production boundary. They are ready for final use – either by consumers or producers

Types:

A. Final Consumer Goods – used by households

Households (people) spend money on final consumer goods.

B. Final Producer Goods – used by firms for investment (not resale)

Producers (businesses) spend money on final goods like machines.

Different Types of Final Goods

1. Used for Final Consumption

Goods bought by customers for personal use.

Example:

- A computer bought to use at home.

- These are called Consumption Goods.

2. Used for Investment

- Goods bought by businesses to use in work or production.

Example:

- A computer bought by an office for employees to work on.

- These are called Capital Goods.

2. Intermediate Goods

- These goods have NOT crossed the production boundary

- Used in further production or resale

Example:

- Shirts bought by Firm X from Firm Y for resale = intermediate goods

- Intermediate Goods are Not included in National Income

- Because their value is already counted in the price of final goods.

Avoid “Double counting"

No Value Addition

When customer buys and eats the bread — it becomes a final good, so no more value is added.

3. Consumption/Consumer Goods

- Directly used to satisfy human wants

- Not used to produce goods and services

Types of Consumption Goods:

- Durable Goods – Long life (TV, Car, Fridge)

- Semi-Durable Goods – Medium life (Clothes, Furniture)

- Non-Durable Goods – Short life (Bread, Milk)

- Services – Intangible (Doctor, Lawyer)

Can Same Goods be Final and Intermediate?

Yes! The same good can be a final good or an intermediate good, depending on who uses it and for what purpose.

It Depends on the Use:

4. Capital Goods

- Used in production of other goods

- High value & long-lasting

- Not directly consumed by households

Examples: Machines, tools, factory equipment

"All capital goods are producer goods, but all producer goods are not capital goods"

Capital Goods

- A type of producer good that is used repeatedly in production.

Examples : Machines, tools, buildings.

Producer Goods

- Goods used by producers to make other goods or services.

Includes both:

- Capital goods (used again and again)

- Single-use raw materials (used once)

Factors of Production

These are the basic resources used to produce goods and services.

1. Land

- Natural things like land, water, forests, minerals.

- It is a gift of nature, not made by humans.

2. Capital

- Tools, machines, and factories used to make goods.

- Helps in producing other things.

3. Labour

- Work done by people.

- Includes physical and mental effort.

4. Entrepreneur

- The person who starts a business.

- They combine land, labour, and capital to make products and take risk.

Factor Payments & Transfer Payments

Circular Flow of Income

It is the continuous flow of production, income, and expenditure between households and firms in an economy.

Two-Sector Economy:

1. Households:

- land, labour, capital, entrepreneur.

- Rent, wages, interest, profits from firms.

- Use income to buy goods/services.

2. Firms:

- Use factor services to produce goods.

- Pay households (factor payments).

- Sell goods back to households.

1. Real Flow (Also called Physical Flow)

i. Flow of factor services from households to

→ Firms (like land, labour, capital)

ii. Flow of goods/services from firms to

→ Households

Measures: Production & growth in the economy

2. Money Flow (Also called Nominal Flow)

i. Flow of money from firms to

→ Households(as rent, wages, interest, profit)

ii. Flow of money from households to

→ Firms (as payment for goods/services)

Measures: Money supply in the economy

Leakage:

- Money that goes out of the circular flow.

- Examples: Taxes,Savings, Imports

- These reduce the total money in the economy.

Injection:

- Money that comes into the circular flow.

- Examples: Government spending, Investments, Exports

- These increase the total money in the economy.

Difference Between Stock & Flow

Economic Territory

Economic Territory (Domestic Territory) refers to the geographical area administered by a government where people, goods, and capital move freely.

Scope of Domestic (Economic) Territory

An economy is more than just the land within a country's borders! It also includes some unique and global elements.

1. Political Boundaries:

- Territorial waters and airspace that belong to a country.

2. Transportation Operations:

- Ships and aircraft operated by residents, even if they travel between countries.

3. International Presence:

- Embassies , consulates , and military bases located abroad still count as part of the home country's economy.

4. Global Resource Activities:

- Fishing vessels , oil rigs , and gas platforms operated by residents in international waters.

Normal Resident of a Country

A Normal Resident is a person or institution who Normally resides in a country Has the centre of economic interest in that country.

Citizen

- A citizen is someone who resides in a country according to the legal provisions of that country.

- It is a legal concept.

- Dual citizenship is possible.

What is National Income?

National Income is the total income earned by the people of a country during one year from all economic activities.

From Production point of view

National Income is the money value of all the final goods and services produced in an economy.

From Income point of view

It is the sum total of all the factor incomes earned by normal residents of a country during one year.

Common Conversions in National Income

1. Gross ↔ Net

Gross = Net + Depreciation

Net = Gross – Depreciation

Depreciation is also called Consumption of Fixed Capital (CFC).

2. Domestic ↔ National

NFIA = Income earned from abroad – Income paid to abroad

National Product = Domestic Product + NFIA

Domestic Product = National Product – NFIA

3. Market Price (MP) ↔ Factor Cost (FC)

NIT = Indirect Tax – Subsidy

Market Price (MP) = Factor Cost (FC) + NIT

Factor Cost (FC) = MP – NIT

Difference Between Depreciation & Capital Loss

Steps to Calculate National Income (Production Method)

Step 1 : Write Sales Value

Add the sales of all sectors (primary, secondary, tertiary) if given.

Step 2: Add Change in Stock

Change in stock = Closing stock – Opening stock (This shows unsold goods added this year)

Step 3: Subtract Intermediate Consumption

- These are raw materials used in production.

- Capital goods are not subtracted (they are not intermediate goods).

- You have reached GDPMP

PRODUCTION (VALUE ADDED) METHOD

Step 1 : Classify Production Units

- Identify and classify all production units into:

- Primary Sector (agriculture, mining)

- Secondary Sector (manufacturing, construction)

- Tertiary Sector (services)

Step 2 : Calculate GVAMP

- Compute Gross Value Added at Market Price (GVAMP) for each sector.

- Add up GVAMP of all sectors to get GDP at Market Price (GDPMP):

- GDPMP = ∑ GVAMP

Step 3 : Calculate Domestic Income (NDPFC)

Subtract Depreciation and Net Indirect Taxes from GDPMP :

NDPFC = GDPMP − Depreciation − Net Indirect Taxes

Step 4 : Calculate National Income (NNPFC)

Add Net Factor Income from Abroad (NFIA) to Domestic Income:

NNPFC = NDPFC - NFIA

Important Formula

GVAMP = Value of Output – Intermediate Consumption

Precautions while Calculating National Income

- Intermediate Goods (used to produce final goods) are not included.

- Second-hand Goods (used items) are not included.

- Services for Self-Consumption (e.g., a doctor treating themselves) are not included.

- Goods for Self-Consumption (like home-grown food) are included.

- Imputed Rent of Own House (house you live in but don't pay rent for) is included.

- Buying & Selling of Shares and Debentures (financial instruments) not included, as they are just paper transactions with no actual production.

INCOME METHOD

Step 1: Classification of Enterprises

Identify and classify all producing enterprises into Primary sector, Secondary sector,Tertiary sector

Step 2: Estimate Total Factor Incomes

Calculate all incomes earned by factors of production (Rent, Wages, Interest, Profit)

These are categorized as:

- Compensation of Employees (COE)

- Operating Surplus (OP)

- Mixed Income of Self-Employed(MI)

Step 3: Calculate Domestic Income (NDPFC)

Add all factor incomes from Step 2:

NDPFC = COE + OS + MI of Self Employed

Step 4: Calculate National Income (NNPFC)

Add Net Factor Income from Abroad (NFIA) to Domestic Income:

NNPFC = NDPFC + NIFA

More Precautions while Calculating National Income

- Transfer Incomes like pensions, donations, scholarships not included (because no production happens).

- Sale of Second-Hand Goods not included (already counted when first sold).

- Sale of Shares & Debentures not included (no production involved).

- Windfall Gains like lottery winnings not included.

- Imputed Value of Services (e.g., owner living in own house) included.

- Compulsory Payments like Gift Tax not included (they are not income from production).

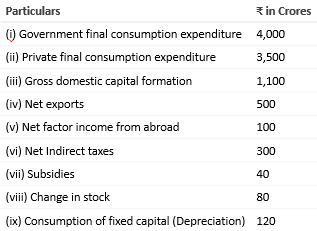

Expenditure Method

Step (i): Identify & classify all the economic units into:

- Household sector

- Government sector

- Producing sector

- Rest of the world

Step (ii): Classify the final expenditures by these sectors:

- PFCE = Private Final Consumption Expenditure

- GFCE = Government Final Consumption Expenditure

- GDCF = Gross Domestic Capital Formation

- Net Exports (X − M) = Exports minus Imports

- The sum of all these = Gross Domestic Product at Market Price

- National Income (NNPFC) = GDPMP− Depreciation + NFIA − Net Indirect Tax

Precautions While Calculating National Income

1. Intermediate Goods Not Included

Only final goods are counted to avoid double counting.

2. Transfer Payments Not Included

Examples: Pensions, scholarships, unemployment allowances.

3.Second-hand Goods Not Included

However, brokerage on second-hand goods is included because it's a current service.

4. Financial Assets Not Included

Example: Purchase of shares, debentures, bonds.

These are just paper claims, not actual production.

5. Production for Self-Consumption Included

Example: A farmer consuming their own crops.

Nominal GDP And Real GDP

Nominal GDP

Nominal GDP is the total value of all goods and services produced in a country in a year, calculated using the current year’s prices.

Real GDP

Real GDP is the total value of goods and services produced, but calculated using constant prices (from a base year).

Difference between Real GDP & Nominal GDP

Conclusion:-

Real GDP is better than Nominal GDP because it gives a more accurate and realistic picture of economic performance.

GDP Deflator / Price Index

- GDP Deflator measures the change in the average price level of all goods and services that make up GDP.

- It is used to eliminate the effect of inflation and helps in determining the real change in physical output.

- It’s calculated as:

Limitations of Using Real GDP as an Index of a Country's Welfare

Real GDP is commonly used to measure a country’s economic performance — but it has some important limitations when used as an indicator of welfare:

Distribution of GDP

- Real GDP ignores the distribution of income.

- Even if GDP increases, economic welfare won’t improve if income is not distributed equitably.

- Unequal growth = Unbalanced welfare

Non-Monetary Exchanges

- Many activities are not recorded in monetary terms — like barter transactions or household work — so they are not included in GDP.

- This leads to an underestimation of actual economic activity and limits GDP’s accuracy as a welfare indicator.

- If it’s not priced, it’s not counted!

Externalities

- Externalities are positive or negative side effects of economic activities that do not involve any payment or penalty.

- Positive Externality: Planting more trees – benefits society, but not included in GDP.

- Negative Externality: Factory pollution – harms society, but no penalty is included in GDP.

- GDP does not reflect these impacts, so it cannot measure true welfare.

Practice important Question

1. Calculation of NDP at FC:

2. Calculation of Domestic Income (NDP at FC):

3.Calculation of National Income (NNP at FC)

4. Calculate Subsidies

An economy has only two firms A and B. On the basis of the following information about the firms, find out:

(a) Value added by firms A and B

(b) GDP at MP (Market Price)

Calculate Net Value Added at Market Price (NVA at MP)

Calculate Net Value Added at Factor Cost (NVA at FC)

Calculate Domestic Income (NDP at FC)

Calculate National Income (NNP at FC)

Calculate GNP at Market Price (GNP at MP)

(a)Gross Domestic Product at Market Price (GDP at MP)

(b) National Income (NNP at FC)

Calculate GDP at Market Price (GDP at MP)

Calculate National Income (NNP at FC)